Are you living paycheck to paycheck and worried you couldn’t cover any unexpected expenses, let alone a full-blown emergency? Is paying the interest on debts straining your monthly budget?

Perhaps the stress of your current situation is starting to interfere with your mood, outlook, and ability to sleep soundly. Maybe it’s always in the back of your mind, like a dark cloud hanging over you every second of every day.

Have you resolved to make some smart money moves this year, but have no idea where to begin? If so, this article is for you!

According to the Bankrate’s annual emergency savings report, published in January of 2024:

- People are attempting to increase their emergency savings and reduce debt.

- Over 30% of those surveyed had higher credit card debt than money saved for emergencies.

- More than 60% of respondents didn’t believe they had enough savings to cover a single month without income.

This data was similar to that of the Barron-Harris poll published in the fall of 2023. More than 60% of participants reported that they were, for the most part, living from paycheck to paycheck.

If you’re ready to improve your financial situation, but are not sure where you should start, follow these steps:

Step 1 – Trim Your Expenses

Review your earnings and expenses. If you can, identify places where you could spend less. This will free up more money for savings, debt repayment, and investments. While you are doing this, calculate your base expenses – what you would need month-to-month if you were ill, unemployed, or unable to work for any other reason.

If you’re already tracking your cash flow, this won’t be difficult. If you don’t currently have a spending plan, check out these articles:

- Budgeting, Beyond the Basics

- Budgeting Blunders – How to Avoid These Five

- Lifestyle-Based Budget: How I Ended Up With One

Step 2 – Save 1 month of Expenses, As a Cushion

Keep an extra month of essential expenses in your checking account. This should ensure it’ll never become overdrawn. And, if and when the funds are needed, they’re immediately accessible.

Once you have padded your bank account, focus on debt management.

Step 3 – Pay off (High Interest) Debt

Tackle loans with high or variable interest rates and any connected to rapidly depreciating assets first.

To learn more about how to approach debt repayment, look over the article Paying Down Debt.

There are multiple benefits of eliminating debt. First and foremost, you stop losing money to interest each month. Cash is freed up in your monthly budget, which you can save and invest. Also, your debt-to-income ratio improves, which impacts your credit score.

Depending on how much you owe, and what type of loans you have, you could decide what portion of available money should be used for debt and how much to continue to direct to savings.

Once you’re down to mortgage debt alone (or home and student loan), and have at least 3 months of base expenses set aside for emergencies, you’ll want to consider paying a little extra each month. Alternatively, you could occasionally make an extra payment.

Because overpayments are applied to the principle, rather than interest, adding a little extra, each month, can significantly decrease the interest paid across the life of the loan. Consequently, you may be able to shave years off the term, to be mortgage (or student loan) free much sooner.

Although this is generally a smart money move, there are a few important exceptions, times when this isn’t the best next step. For instance, not all lenders allow overpayment. Some lenders, conversely, let you pay more than required but charge a fee when you do.

When deciding whether it’s advantageous to pay extra, the remaining balance of a debt matters. This is a particularly important factor when loans are amortized, since the amount going to interest is decreasing, over time. For these loans, the biggest bang for your (overpayment) buck occurs in the beginning, then decreases over time.

At some point, as the portion going to interest gets lower, the number of equally good, or better, opportunities elsewhere grow. That is, unless you are close enough to the end of the loan that you could eliminate the debt altogether and, along with it, a substantial monthly payment.

After debts are eliminated, or at least under control, it’s time to set more money aside for emergencies.

Step 4 – Save 3 to 6 months of Unavoidable Expenses, in case of Emergency

Emergency funds are based on expenses that wouldn’t go away following a catastrophic financial event (ex: utilities, health insurance premiums). You don’t need to include any areas of average monthly spending that would no longer be needed or prioritized (ex: streaming services, gas to and from work).

There are ways to calculate emergency fund needs more precisely, but the general rule is 3 to 6 months of base expenses. People in specialized fields might need to set more aside. This is especially important if it would take longer than 6 months to find and start a new job. Another relevant consideration is your long-term disability policy’s elimination period.

Investopedia has a helpful article on the topic – Elimination Periods in Disability Insurance: How They Work.

Emergency money, unlike the cushion, should be held in a money market fund or high-yield savings account. These types of accounts will earn more interest. To maintain purchasing power, funds must earn enough interest to exceed the (current or average) inflation rate.

To learn more about the importance of “beating inflation”, read Why Hiding Money Under Your Mattress Isn’t the Best Idea.

Once you’ve set aside a full three months of emergency savings, you can shift some of your discretionary cash flow toward your long-term financial objectives.

Hopefully, even when your main priority is something else, you’ll grab opportunities, here and there, to throw money into your emergency fund. Think of saving as both an individual step in this process and a thread that cuts across it.

You may have found yourself having to dip into your emergency fund for things that didn’t quite qualify as an urgent situation. Perhaps you had an unexpected or larger than average expense. Maybe you drew from these funds to go on vacation or buy a new car.

It’s time to start saving for things that can be planned for, separately. This will leave your emergency savings untouched, available for more extreme life circumstances, which couldn’t have been predicted.

Step 5: Contribute to Retirement

While you continue to build your emergency fund, beyond the first 3 months, start saving for retirement. The smart money strategy is to begin saving for retirement sooner, rather than later.

When it comes to investing, time is a vital factor. Staying invested for long periods of time lets people take advantage of compound interest. To oversimplify, this occurs when reinvested interest creates additional interest…

Compound interest is the eighth wonder of the world.

Those who understand it, earn it;

those who don’t, pay it.

adapted from Albert Einstein

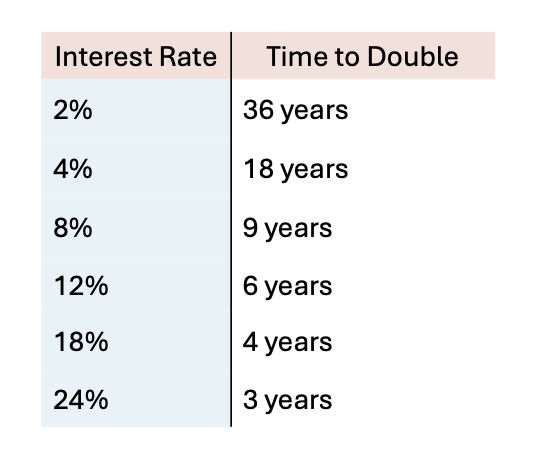

To begin to understand the impact of this smart money phenomenon, you can fiddle with a compound interest calculator. Alternatively, the rule of 72 is used to calculate how long it takes investments to double at various interest rates.

If you’d like to understand the math behind the rule, watch this video from Khan Academy.

There is no mandate saying you have to max out your retirement accounts. Start small, then scale up over time. For now, add what you can afford. Then, as you continue to cut expenses and eliminate debt, increase your contributions.

Try to set aside enough to receive any free money (matching money) your employer is willing to contribute. If, on the other hand, your employer doesn’t provide a match, 3 to 5% might be a good starting percentage.

If your employer doesn’t have a retirement plan, you can open Individual Retirement Accounts (IRAs) through a brokerage firm. There are multiple retirement plans available for small businesses, solopreneurs, and other variations of self-employment. Carefully consider the advantages and disadvantages of each type. To be smart with money, we need to create our own financial solutions from time to time.

Choosing a Retirement Solution for Your Small Business, a joint project of the U.S. Department of Labor’s Employee Benefits Security Administration (EBSA) and the Internal Revenue Service, is a helpful resource.

Step 6 – SavE & Invest

To truly be smart with our money, we must think past (and beyond) the emergency fund. This may be a huge mindset shift – from buying then paying off, to saving then buying.

More people should learn to tell their dollars where to go

instead of asking them where they went.

Roger Babson

Non-emergency savings includes needs (ex: a new phone sometime next year), occasional but predictable larger expenses (ex: downpayment for a house), as well as items from your wish list (ex: a new bicycle) and bucket list (ex: trip to Europe).

Funds for wants, needs, and financial goals (other than retirement) that will not be happening in the next year, or so, can be invested until they’re needed. Where the money is invested may depend on what it’s being used for. For instance, children’s educational savings can be put in a 529 plan. Money for medical expenses, on the other hand, might be contributed to an HSA or FSA account. Note that not everyone is eligible for an HSA and that FSA funds, for the most part, don’t carry over from year to year.

Once you’ve reached this step, you have really turned your situation around. You’re reasonably financially stable, and have put systems into place that have and will continue to lead to positive financial outcomes. Whether you’ve realized it or not, you’re no longer trying to get by, struggling, and stressing. You’re building wealth!

So, why is there a step seven? Although your financial future is predicated on whether you are falling behind, breaking even, or getting ahead (month to month), there are things that either slow down or speed up that process. And, of those things, having a comprehensive plan is arguably the most important.

Step 7 – Design a Comprehensive Financial Plan

Being smart about money involves not just accumulating but also protecting your assets. It’s not difficult to find a story where someone, in an instant, lost everything they’d spent years working for. That is, unfortunately, something that can happen if you don’t have the right insurance policies in place.

Having a high investment rate is wonderful, but if portfolio allocation isn’t carefully considered, you may be taking on more risk than you’re willing or able to. And, although in the beginning you probably put whatever you could afford into savings and investments, at some point you’ll want to estimate, more precisely, how much you need to deposit into each account to reach your goals in a timely fashion.

Finally, there’s the question of what you’ll do with the money you’ve saved while in retirement. Are you planning to spend it all? Or will you leave some behind for your loved ones? Do you have an estate plan in place that will ensure your wishes are fulfilled?

To learn more about leaving a legacy, read Estate Planning – A Guide

I always have mixed feelings about including step seven, because I see it less as the final step in the quest for financial stability, and more as the first step in intentional, effective wealth building.

Subscribe for thoughtful notes on money, meaning, and designing a life that’s uniquely you — delivered straight to your inbox.

What to Read Next

If this idea struck a chord, you might enjoy these related reflections:

The Psychology of Investing — 8 Takeaways

Digital, Financial, and Nutritional Detox: Reclaim Your Life